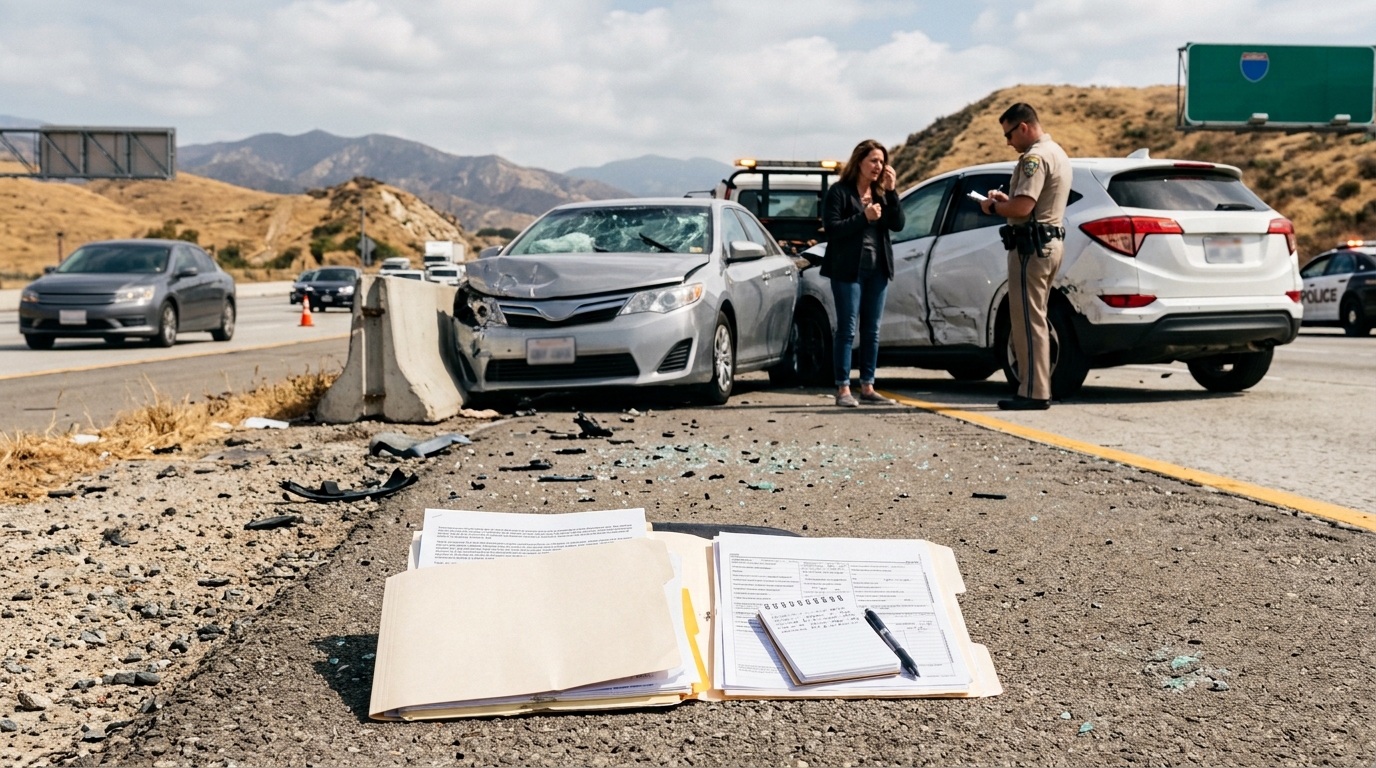

California minimum auto insurance limits in 2026 are an important issue for anyone injured in a car accident. Many drivers hear that the state raised the required liability limits and assume that serious accident victims now have enough coverage available. That assumption can be dangerous. The new limits are higher than the old requirements, but they can still fall short when a crash causes emergency treatment, surgery, lost income, long-term pain, or multiple injured people.

California now requires most drivers to carry at least $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage. These limits are often called 30/60/15. They are better than the old 15/30/5 minimums, but “better” does not always mean “enough.” A single ambulance ride, emergency room visit, imaging bill, specialist consultation, and physical therapy plan can quickly create expenses that push against the available insurance.

This is why accident victims should not evaluate a case only by asking whether the at-fault driver had insurance. The better question is whether there is enough insurance to cover the full harm. In many serious claims, the answer may be no. That is where evidence, medical documentation, uninsured and underinsured motorist coverage, and careful settlement strategy become critical.

This article is for educational purposes only and is not legal advice. Every accident claim depends on the facts, insurance policies, injuries, and deadlines involved.

What California’s 30/60/15 Insurance Limits Mean After a Crash

The phrase 30/60/15 sounds technical, but the basic meaning is simple. The first number, $30,000, is the minimum bodily injury coverage available for one injured person when the insured driver causes a crash. The second number, $60,000, is the minimum total bodily injury coverage for all injured people in one accident. The third number, $15,000, is the minimum property damage coverage.

For accident victims, the most important part is the gap between insurance limits and real losses. If one person suffers a serious injury, $30,000 may not cover the medical bills, lost wages, and pain caused by the crash. If three or four people are hurt in the same collision, the $60,000 total limit may need to be divided among all valid injury claims. That can leave each person with far less than the value of their damages.

For official background, the California DMV explains the state’s current minimum liability insurance requirements here: California DMV Auto Insurance Requirements.

Minimum coverage is not the same as full compensation

One of the biggest mistakes after a crash is assuming that the available insurance automatically equals fair compensation. Minimum coverage is only the legal floor. It is not a promise that the policy will cover the full cost of an injury. A crash victim may have hospital bills, follow-up care, missed work, reduced earning ability, medication costs, vehicle damage, and pain that lasts for months or years.

Your existing guide on Car Accident Compensation: How Much Can You Really Get? is a useful internal link here because it explains how claim value depends on more than the policy limit. Injury severity, medical expenses, lost income, liability, and pain and suffering all affect the final value.

Medical bills can exceed the policy quickly

A driver with minimum insurance may technically be legal, but that does not mean the policy can handle a major injury claim. Emergency care alone can be expensive. Add surgery, orthopedic care, neurological symptoms, injections, therapy, or time away from work, and the available $30,000 per-person limit can become a serious problem.

This is especially true in crashes involving motorcycles, pedestrians, cyclists, high-speed impacts, commercial vehicles, or severe rear-end collisions. The body can suffer damage that is not obvious at the scene. That is why early medical care and consistent follow-up matter. Treatment records show not only what happened medically, but also why the claim may be worth more than the available minimum policy.

Multiple victims may have to share one limit

The $60,000 per-accident bodily injury limit can create another problem. If several people are hurt, that total coverage may need to be shared. For example, two injured occupants may both have hospital bills. A pedestrian and a passenger may both have claims. A family inside one vehicle may have several injured members. In those situations, the insurer may not simply pay one person the full policy without considering other claims.

When multiple claimants are involved, settlement timing and documentation become even more important. Victims should avoid assuming the insurer will voluntarily explain every available option. The insurance company’s job is to resolve exposure within the policy, not to build the strongest possible case for the injured person.

Property damage limits can also create pressure

The $15,000 property damage minimum is also not always enough. Modern vehicles can be expensive to repair, especially when sensors, cameras, safety systems, bumpers, airbags, or frame components are damaged. A newer vehicle may suffer repair costs that exceed the property damage limit even when the injury portion of the claim is still unresolved.

Property damage pressure can also affect the injury case emotionally. Victims may need transportation, repairs, towing, rental reimbursement, and help dealing with a total loss. It is easy to focus on the car first because that problem is visible every day. But if there are injuries, the medical claim usually needs more careful attention than the vehicle claim.

Do not settle the injury claim just to finish the car claim

Insurance companies may try to move quickly when damages appear small. That can be fine for a minor property-only crash, but it becomes risky when injuries are still developing. Once an injury claim is fully released, the victim may not be able to reopen it later just because symptoms worsened or new medical bills appeared.

Before signing anything, injured people should understand what is being released. A property damage settlement and an injury settlement are not always the same thing. If the document releases all claims, it may end the injury case too. That is why accident victims should read settlement paperwork carefully and avoid rushing.

How Accident Victims Can Protect a Claim When Insurance Is Not Enough

When California minimum auto insurance limits in 2026 are not enough to cover a serious crash, the injured person needs a broader strategy. The claim should not stop at the first policy limit. Instead, the victim should look for every available source of recovery and preserve evidence before it disappears.

Possible sources may include the at-fault driver’s policy, the victim’s own uninsured or underinsured motorist coverage, another liable driver, an employer-owned vehicle policy, a commercial policy, a rideshare policy, or other responsible parties depending on the facts. Not every case has multiple sources, but serious cases should be reviewed carefully before the victim assumes the minimum policy is the end of the road.

UM and UIM coverage may matter more in 2026

Uninsured motorist coverage may apply when the at-fault driver has no insurance. Underinsured motorist coverage may apply when the at-fault driver has insurance, but not enough to cover the damage. These coverages can become extremely important when the at-fault driver only carries the California minimum.

For related reading, see Hit-and-Run Accidents in California: How UM/UIM Coverage and Fast Evidence Collection Can Protect Your Claim in 2026. Even though hit-and-run cases are different, the insurance lesson is similar: your own policy may become a major part of the recovery plan when the other side cannot fully pay.

Evidence still controls the value of the claim

Insurance coverage matters, but evidence still drives the claim. A victim should preserve photos, videos, police report details, witness names, repair records, medical bills, diagnosis notes, work restrictions, and proof of lost income. If the crash involved a newer vehicle, dashcam footage, event data recorder information, or telematics may also matter.

Your article on California Dashcam and Black Box Evidence in 2026 fits naturally here because a low-limit policy makes evidence even more important. If the available insurance is limited, the victim cannot afford weak proof, missing records, or a sloppy timeline.

Victims should also review the basic steps in What to Do After a Car Accident: A Step-by-Step Legal Guide and The Ultimate Guide to Filing a Personal Injury Claim. Those guides support the bigger point: the first days after a crash can shape the strength of the entire case.

California’s higher minimum limits are a step forward, but they do not eliminate the financial risk of serious crashes. A minimum policy may still be too small for surgery, permanent injury, multiple victims, lost income, or long-term treatment. Injured people should not confuse legal minimum coverage with full compensation.

If you were hurt in a California accident in 2026, focus on medical care, evidence preservation, insurance review, and timing. The at-fault driver’s policy may be only one part of the recovery picture. The stronger your documentation is, the better chance you have of protecting the value of your claim when the available coverage is limited.